By Kerry Pivovar:

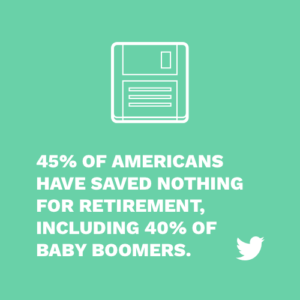

It’s never too late to start discussing retirement. While situations among the working can be vastly different, the one common things we hear is- you can never have enough retirement planning. In 2017, 70% of civilian workers and 94% of union workers had access to retirement and medical benefits, yet 45% of Americans have saved nothing for retirement, including 40% of Baby Boomers. This shows just how much of an underutilized benefit employer-sponsored retirement plans are among most employees.

High participation in a #retirement plan can lead to improved #retention, increased loyalty and employee buy-in. Use these 5 tips to increase enrollment! Click To TweetDiscussing the retirement plan during onboarding is not enough. Not all employees have enough financial education to confidently kickoff this account. While it may feel out of the realm of company responsibilities to help employees with their life after work, the benefits to both the organization and employee can’t be overlooked. Showing interest in how your employees are using or not using the fund is a way to set yourself apart in a competitive recruiting landscape. Employees want to see companies give a more holistic approach to workforce support. A healthy employee isn’t just engaged at work, but also secure and independent outside of the office. High participation in a retirement plan can lead to improved retention, increased loyalty and employee buy-in. As participation increases, plan fees diminish freeing up cash to reinvest in the company.

50 great benefits you don’t know you’re offering

All this in mind, how exactly can an organization encourage and increase participation?

1. Explain the Situation

A good rule of thumb is to have 10 times your final salary in savings if you want to retire by age 67. Walking through the retirement planning landscape with your employees is the first step in plan participation. Even if only 1% of income is set aside, contributing at all is a move in the right direction.

It shows foresight and self-discipline on the way to overall financial health. Explain this to your employees! Show them the powers of compound interest, how much they may need upon retirement and the current state of Social Security.

One of the most misunderstood concepts of a retirement plan is the tax structure. An IRA is not simply a savings account. The tax structure alone sets these plans apart from bank accounts. Money designated for the plan comes out as pre-tax income. Meaning a set percentage of your paycheck before tax can be set aside in the plan. This shelters your money from the federal and state taxes applied to the rest of your paycheck (for now). Three common types of plans include 401(k), 403(b) and Simple IRA.

Learn more about how taxes affect retirement accounts

401(k): With a Traditional version of the 401(k), your money is contributed before taxes, meaning that you receive a tax deduction that lowers your income, or in other words, you have a lower tax liability now. However, in the future, when you withdraw your money from your account, you have to pay income taxes on the amount you withdraw.

403(b): The 403(b) is set up similarly to a 401(k) but offered to state employees and non-profit employees.

SIMPLE IRA: A Simple IRA is an employer-sponsored retirement plan offered within small businesses that have 100 or fewer employees. Contributions to the plan are made pre-tax, and the money in the plan accumulates tax-deferred until the money is withdrawn at retirement.

These accounts when invested will benefit from compound interest. So…what exactly is compound interest, you ask?

“Compound interest is interest paid on the initial principal as well as the accumulated interest on money you have borrowed or invested. Compound interest is like double chocolate topping for your savings. You earn interest on the money you deposit, and on the interest you have already earned – so you earn interest on interest.”

Benefits that blow

2. Auto Enrollment

A survey from Alight Solutions found that 68% of large U.S. employers now auto-enroll their employees. One of the most effective ways to increase employee participation is to automatically enroll new employees. Requiring them to opt-out instead of opt-in makes it easy. Studies show that many employees choose not to enroll because they are confused by the process.

“Automatic features harness the power of inertia by taking the workers who may not take action and making sure that they begin to save today for retirement. This helps increase the chance that more people will be on a favorable path to a more secure financial future.”

–Rob Austin, director of Research at Alight.

Auto-enrollment should be a well-known fact to your employee right away. Finding out a certain percentage of money was held back from an employee’s paycheck without them realizing can cause distrust and anger. Clearly explain what is happening from day one so employees know they the choice to continue or easily opt-out.

3. Offer an Employer Match

Employees choose to set aside a chosen percentage to invest into their retirement plan. Employers can choose to match up to a certain percentage to enter the account. (Employers do not have to offer this benefit when setting up plans.) Companies that offer matches have the chance to provide free money to employees receiving a tax break in return. A match can inspire employees to contribute in order to receive the full match. An employer match is a powerful benefit that can accelerate savings. In return, watch employees loyalty and engagement rise.

Employees choose to set aside a chosen percentage to invest into their retirement plan. Employers can choose to match up to a certain percentage to enter the account. (Employers do not have to offer this benefit when setting up plans.) Companies that offer matches have the chance to provide free money to employees receiving a tax break in return. A match can inspire employees to contribute in order to receive the full match. An employer match is a powerful benefit that can accelerate savings. In return, watch employees loyalty and engagement rise.

Consider adding a student loan repayment program to your benefits

4. Automatically Increase Employee Contributions

A progressive way to increase employee contributions is to automatically increase the contribution. This feature one, along with auto-enrollment must be clearly communicated to your employees. Auto-escalation increases a participant’s deferred rate of 1% every year until they reach a predetermined cap (usually 10%). Just as salary is re-evaluated every year, retirement plans should be as well. If an employee is earning more money, she should think about increasing her contribution, however, this step is often overlooked. Automatically increasing contributions does this for you without having to think about it.

5. Offer Continued Education

“You must gain control over your money or the lack of it will forever control you.”

–Dave Ramsey

Provide education regularly to your employees. There is always more that can be done to increase preparedness. Emergency funds, separate investment accounts, Roth IRAs, the list goes on. Whether it’s offering a seminar on personal finance, establishing a financial wellness program or starting a small library of books and resources, keeping employees apprised of their money can be a life-changing benefit. Even if your employee chose not to participate in the retirement plan day 1, over time using the financial education provided he is now confident to sign up in year 2.

How to start a financial program at your company

Long-term Success

The average American retires at age 63. It’s never too early to start thinking about greener pastures. Any financial advisor will tell you starting young is one of the most powerful tools in investing. You’ve done the first step in offering a plan to your team. Now, using these five steps, employee participation in your retirement plan will increase setting up your company and the employee up for success long-term.

Related Posts

6 Minute Read

6 Minute ReadThe First Date Principle: Why Bidirectional Communication is the Heart of Meaningful Sales and Marketing

12 Minute ReadGive Voting a Chance

9 Minute Read